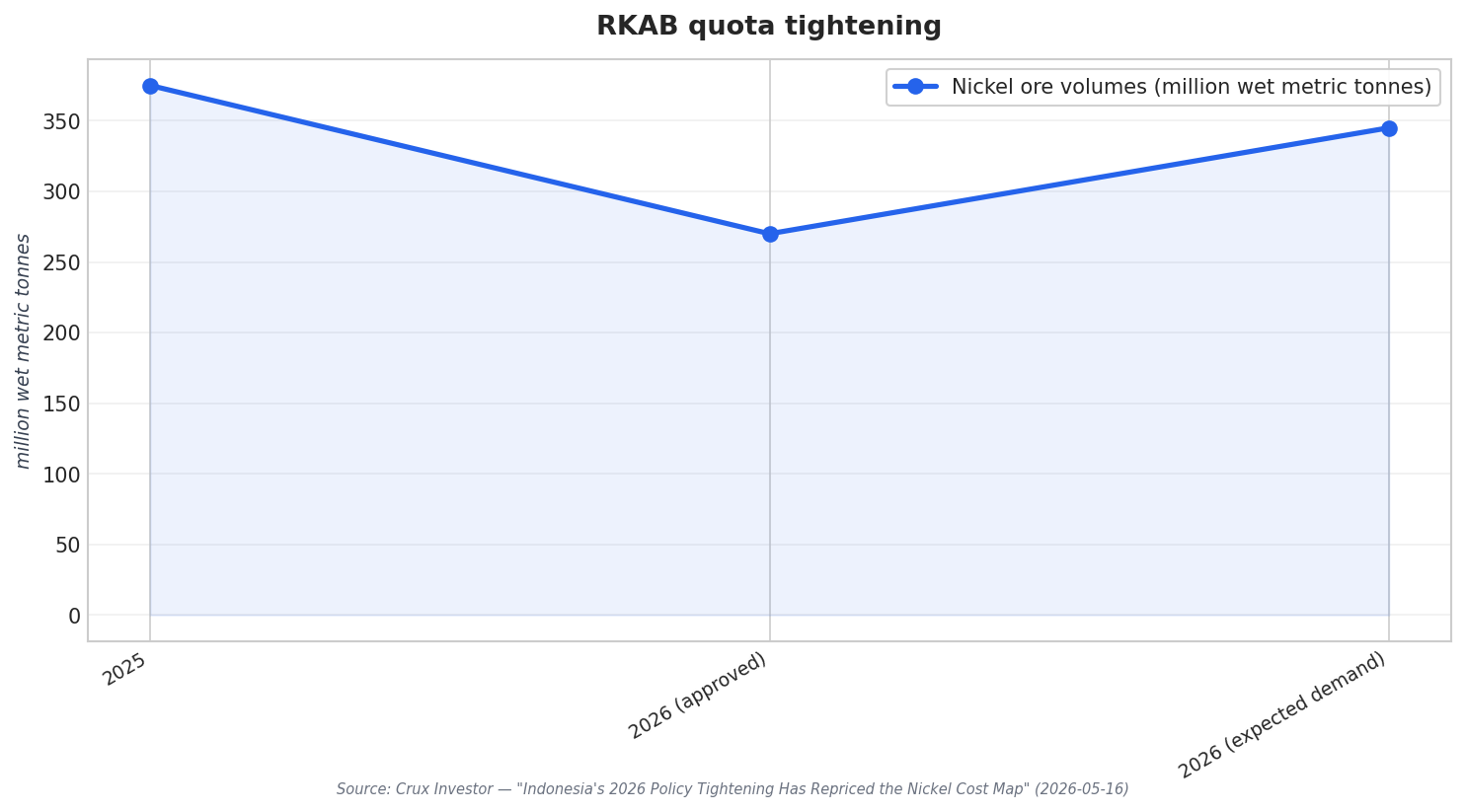

Indonesia’s 2026 RKAB nickel ore quota is now a central issue for downstream investors because it narrows the feedstock pipeline that many processing projects rely on. Crux Investor reported an approved 2026 RKAB allocation of 270 wet metric tonnes, down from 375 wet metric tonnes in 2025, and short of expected demand of 345 wet metric tonnes. Argus framed the cut similarly, noting the reduced quota is about one-third lower than the 2025 approved quota of 379mn t and significantly below its forecast 330mn t of Indonesian nickel ore consumption for 2026. For capital tied to processing build-outs, that gap matters because downstream utilisation ultimately tracks ore availability, not nameplate ambition.

The immediate market response has already shown how quickly Indonesian supply decisions can reprice expectations. Goldman Sachs said nickel climbed sharply amid a broader metals rally, with the base metal jumping more than 30% between mid-December and January. Argus reported LME nickel prices spiked to a 1½-year high of $18,950/t on 29 January, supported by geopolitical tensions and Indonesia’s intent to reduce ore supply. Crux Investor separately noted the LME nickel price rallied 37% from late December 2025 to April 2026. These moves reinforce the point from Goldman Sachs that Indonesia is the “lever the market is watching,” especially given its share of more than 60% of global nickel mine supply.

Why 2026 Tightening Hits HPAL Costs Harder Than Many Models Assumed

For HPAL-focused downstream investors, the quota debate is only half the story. Crux Investor highlighted two interdependent cost vulnerabilities for Indonesian HPAL operations: reliance on imported sulphuric acid and progressively declining domestic ore grades. It reported that the closure of the Strait of Hormuz and a Chinese sulphuric acid export ban drove high acid prices and the risk of market shortages, raising input costs for Indonesian HPAL producers that cannot source the reagent domestically at scale. It also noted that ore grades falling below 1.5% increase acid consumption per unit of nickel recovered due to a fixed chemical relationship in the HPAL process, compounding reagent pressure that operational efficiency cannot fully solve.

This is where Indonesia’s nickel downstreaming policy becomes more than a processing mandate and turns into a new cost map for investors. Crux Investor said the quota decision came alongside a revision to the HPM benchmark pricing mechanism and increases to tiered royalty rates, contributing to a higher structural cost floor for HPAL production. Goldman Sachs echoed the idea of a higher cost floor, explaining that marginal production costs are now higher than it was forecasting last year, and it raised its 2026 forecast by 16% to an average $17,200 per tonne (from $14,800 per tonne in January). In early February, it noted nickel traded at $17,040 on February 16.

Investors are also watching whether quota discipline persists through 2026 because that determines whether tightening is viewed as an anomaly or a baseline. Discovery Alert argued that if Indonesia maintains a 260–270 million ton quota through year-end without significant supplementary allocations, the global market could move from structural surplus toward near-balance or mild deficit in H2 2026. Crux Investor reported the INSG revised its 2026 balance from a 283,000-tonne surplus to a 32,000-tonne deficit, reinforcing the idea that the market is pricing tightening as durable rather than temporary. For downstream investors, the practical signals to track include official RKAB approvals, LME inventory trend direction, and smelter utilisation rates at Morowali and Weda Bay, as highlighted by Discovery Alert.

What is Indonesia’s 2026 RKAB nickel quota, and how does it compare with 2025?

Why does the quota tightening matter so much for downstream investors?

How did nickel prices react to Indonesia’s tighter supply signals?

What risks are specific to HPAL projects in Indonesia right now?

How does Indonesia’s nickel downstreaming policy shape investment behavior in 2026?