Foreign investors are paying attention to Indonesia’s waste-to-energy push because Danantara is packaging it as a repeatable, financeable program rather than a one-off plant. Danantara’s leadership has said it is pursuing waste-to-energy facilities nationwide in tranches, starting with a first batch in seven priority cities. Those cities include Bali, Bogor, Tangerang, Semarang, Medan, Bekasi, and Yogyakarta. The program is explicitly framed as an answer to visible waste problems that affect tourism, and President Prabowo Subianto has urged Danantara to launch soon. For investors, the combination of political urgency, a defined city pipeline, and a standardized approach reduces ambiguity when assessing project readiness.

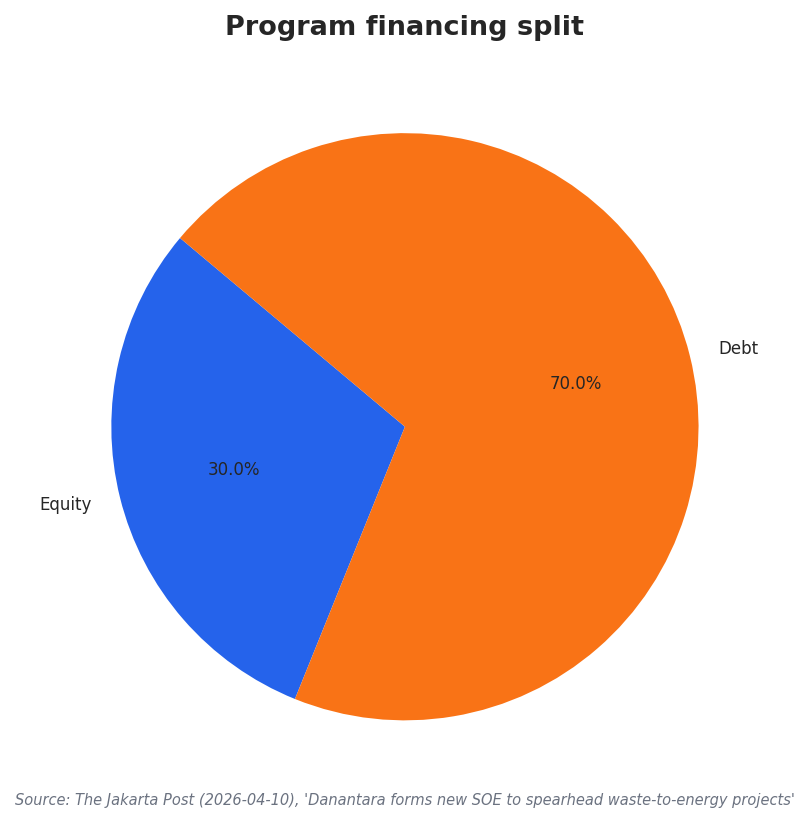

Another draw is the way Danantara describes ownership and risk sharing. Chief investment officer Pandu Sjahrir said Danantara wants to hold at least a 30 percent stake in each project, while remaining flexible if partners prefer Danantara to take 51 percent or more. Indonesia is also seeking debt financing to cover 70 percent of costs, with the remainder from equity. That model appears repeatedly across reports: individual plants are cited at Rp 2.5 trillion to Rp 3.2 trillion in investment needs, and each facility is planned to process over 1,000 tons of waste a day. Pandu also described the internal rate of return as “high single digit,” a point that helps explain why lenders and developers keep circling the program.

What Makes the Program Bankable for International Capital

Foreign interest also reflects the volume and structure behind the national plan. The waste-to-energy initiative aims for 33 plants worth a combined Rp 91 trillion, and Danantara has created a dedicated vehicle to centralize execution. The Jakarta Post reported that Danantara established PT Daya Energi Bersih Nusantara (Denera) on April 1 as a holding entity for all waste-to-energy projects, designed to centralize investment, development, and operations. Danantara’s waste-to-energy lead, Fadli Rahman, said Denera will control both equity stakes and operations for all Danantara-owned waste-to-energy assets. This kind of platform structure can make diligence easier for outsiders, because it clarifies who operates assets and how governance is managed across multiple sites.

The tender and partner pipeline is another reason the program keeps attracting cross-border attention. SUPRA International reported that the first batch tender for seven priority cities launched on November 6, 2025, attracting 240 investor registrations, including 24 pre-qualified international companies. Jakarta Globe also said Danantara short-listed 24 companies as technological partner candidates and noted that foreign companies dominated the list, while acknowledging lender interest from Singapore, Japan, China, and Europe. Indonesia Business Post added that 24 foreign companies from China, Hong Kong, France, and Japan entered the first-stage tender. Tempo separately reported that Danantara’s CEO said over 204 foreign investors were interested in the project, reinforcing the depth of the opportunity set.

Finally, the financing story has multiple hooks that appeal to both lenders and equity partners. Danantara has said it still plans to use a portion of proceeds from fully subscribed “patriot bonds,” with a stated aim to raise around Rp 50 trillion (US$3 billion). SUPRA International described an overall financing framework where equity needs approximate IDR 27.3 trillion, representing 30 percent of the IDR 91 trillion program, alongside project finance debt totaling IDR 63.7 trillion. It also stated Danantara would commit minimum 30 percent direct equity participation (IDR 8.2 trillion), with the remaining equity coming from private developers and technology providers selected via competitive tender. In this context, the Danantara waste-to-energy investment narrative becomes straightforward: defined ownership, hybrid funding, and an expanding platform that Danantara has also discussed potentially listing by 2028.

Why are foreign lenders and investors interested in Danantara’s waste-to-energy program?

How many plants are planned and what is the total program value?

What is the typical cost and waste-processing scale of each facility?

What is Denera and why does it matter for investors?

How does the Danantara waste-to-energy investment model split funding and ownership?